The world of finance has historically been an uneven playing field for men and women. As we learned in our recent book club Sapiens: A Brief History of Humankind by Yuval Noah Harari, that “at least since the Agricultural Revolution (12 thousand years ago), most human societies have been patriarchal societies that valued men more highly than women…. Patriarchal societies educate men to think and act in a masculine way and women to think and act in a feminine way, punishing anyone who dares cross those boundaries.” (Page 152). Researchers remain puzzled and haven’t been able to come up with a reason why societies across the globe were patriarchal for at least 12 thousand years. One thing is for sure: women have made more progress in the last century than in the previous 11,900 years combined.

While the gender pay gap has narrowed tremendously over the last century, it has remained relatively stable for the past 15 years, hovering around 82 cents on the dollar.1 This is a surprising statistic, especially knowing that more women graduate from four-year colleges and universities than men and that women make up 50% of the labor force. So, what, then, is going on here?

Despite tremendous progress in recent history, “the events of 2020 have turned workplaces upside down.”2 Women, particularly women of color, were laid off or furloughed at a higher rate during the pandemic, which is putting both their careers and financial security in jeopardy. Left with few options, many women who were lucky enough to keep their jobs this year have considered downsizing their careers to play a bigger role at home. Today, we think it’s as important as ever for women to take control of their finances and make their own decisions when it comes to managing their, and their household’s, money.

Due to a wide variety of factors relating to inequality, historically women have had to work harder and save longer to get to the same financial place as men. While there are many large scale, systematic changes that can help alter these statistics, we have found that there are also a few small steps that women can take to put themselves on the right path to make their financial future more secure.

Learn to be smart with your money. Living within our means doesn’t mean budgeting to spend what we earn. To create a proper budget, we must also include the amount of money that we need to set aside each month for our retirement. This also means we need to be smart with our savings and learn how to invest them. “While stock market downs are definitely a reality, there’s also a risk in being too cautious. Not investing in the stock market can mean missing out on long-term gains that can help you achieve your goals.” –Carrie Schwab-Pomerantz.

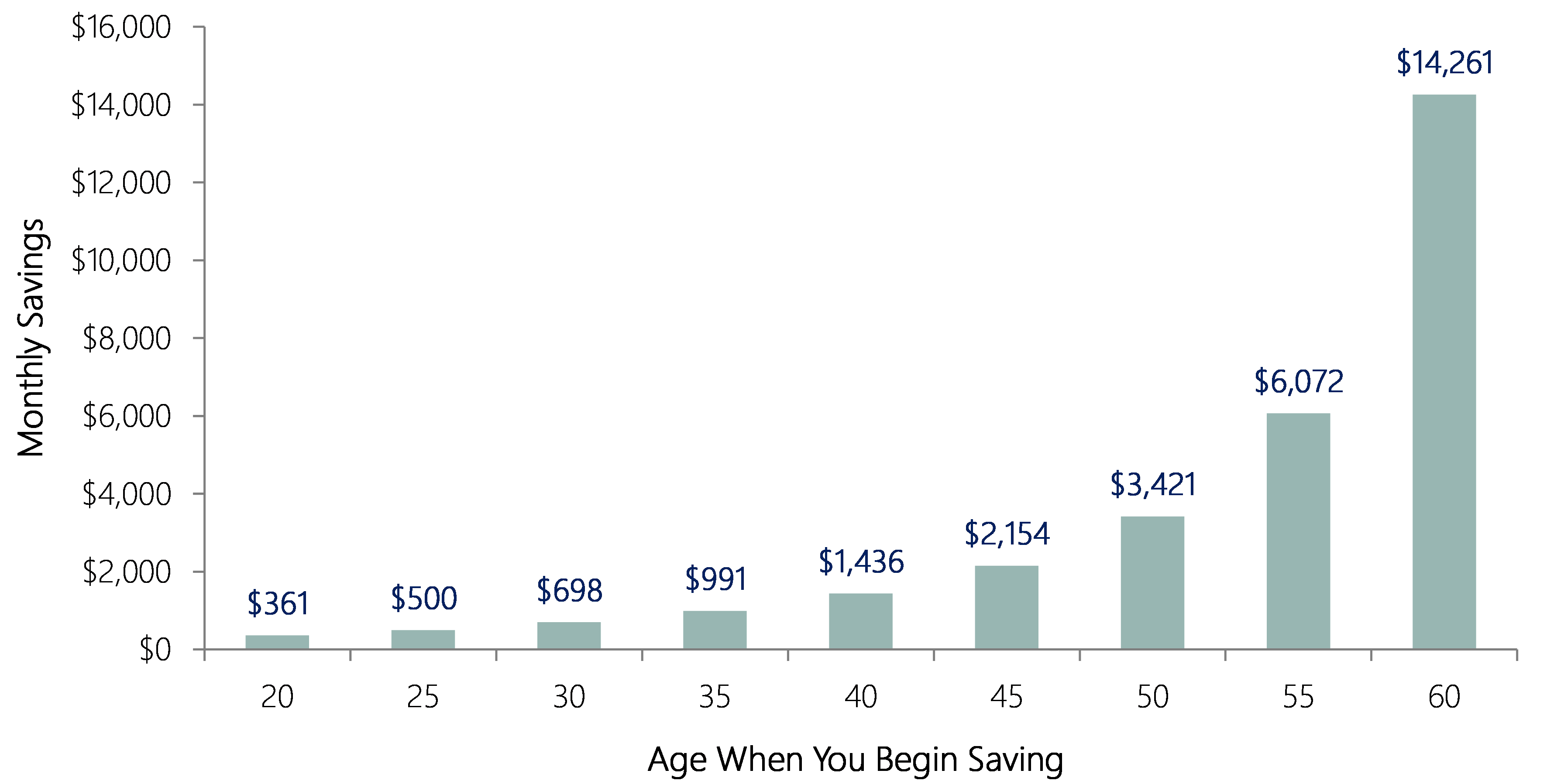

Start planning for retirement early. On average, women live 5 years longer than men in the United States (7 years globally)3 so they must stretch their retirement savings over a longer time span or save more to cover those years. However, on average the median household retirement savings for women is $23,000 versus $76,000 for men. Wow! That is a huge difference! Our tip is to start saving early! The sooner you start thinking about retirement and putting money away, the better off you will inevitably be. We know what you’re thinking: why focus on that when retirement feels so far away? Because the younger you start to save, the less monthly savings you will have to put aside to reach your retirement goals. Don’t believe us? Check out the chart below!

Confidence is key! A study by Merrill Lynch showed that women are much less confident in their investment knowledge than men, citing that 52% of women felt strongly about their investment abilities compared to a whopping 68% of men.4 However, Fidelity found that women actually outperformed men in the last decade of investment returns (2006 to 2016)!5 Why? Because men tended to buy and sell stocks more often to try to time the market and women were more likely to hold course for the long term. It looks like we need to work on changing those confidence statistics!

Be the driver, not the passenger. Over 50% of married women defer to their husbands when it comes to long-term financial decisions, such as estate planning, insurance, investing, and long-term care.6 But in reality, women typically call the shots when it comes to household budgets, even if they don’t realize it: where the kids go to school (public vs. private), what car the family buys, what house they buy, etc. If you are already comfortable making many financial decisions for your family, we suggest stepping into the driver or co-driver seat when it comes to your family’s long-term financial decisions.

Work with a financial advisor to come up with a long-term plan. Having a trusted confidant to bounce ideas off and talk things through with is helpful for us in so many different circumstances, it only makes sense that we have someone like this to help us with our finances. An outsider’s knowledge and perspective can help offer an objective, unbiased opinion, which is an important step in coming up with a financial plan to set us up for success for the long term. Asking questions early and often for clarity and understanding is an important step in this process.

Article Sources:

1. https://www.today.com/tmrw/why-gender-pay-gap-statistics-tell-incomplete-story-t211655

2. https://www.mckinsey.com/featured-insights/diversity-and-inclusion/women-in-the-workplace

3. https://www.health.harvard.edu/blog/why-men-often-die-earlier-than-women-201602199137

4. https://www.forbes.com/sites/tedknutson/2018/04/19/women-much-less-confident-about-investing-than-men/?sh=45c885475f7f

5. https://money.cnn.com/2017/03/08/investing/women-better-investors-than-men/index.html

6. https://www.barrons.com/articles/women-still-arent-managing-their-money-whats-holding-them-back-51607119739

Garrison Point Advisors, LLC doing business as “Treehouse Wealth Advisors” (“TWA”) is an investment advisor in Walnut Creek, CA registered with the Securities and Exchange Commission (“SEC”). Registration of an investment advisor does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. TWA only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of TWA’s current written disclosure brochures, Form ADV Part 1 and Part 2A, filed with the SEC which discusses among other things, TWA’s business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

Certain hyperlinks or referenced websites, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top-level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with TWA with respect to any linked site or its sponsor, unless expressly stated by TWA. Any such information, products or sites have not necessarily been reviewed by TWA and are provided or maintained by third parties over whom TWA exercises no control. TWA expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

Schedule a 30-minute conversation to get started.

Please fill out the form to gain access to the webinar.

Please fill out the form to gain access to the webinar.

Please fill out the form to gain access to the webinar.

Please fill out the form to gain access to the webinar.

Please fill out the form to gain access to the webinar.